Deciding how and when to claim Social Security benefits is one of the most important retirement income decisions you will ever make. The idea of guaranteed income for life that keeps pace with inflation should make you very motivated to learn and understand the various factors that determine how much you get and when.

The first baby boomers reached 65 in 2011, and the remaining 78 million people born between 1946 and 1964 will continue to turn 65 at a rate of 10,000 people per day for the next 15 years.

Social Security is the single largest source of income for the majority of Americans over 65 and represents half or more of total income for 53% of married couples and 74% of unmarried individuals. For more affluent retirement aged people, informed decisions about how and when to claim Social Security benefits can mean thousands of extra retirement income dollars per year. With the right planning a married couple could increase their lifetime income by $100,000 or more.

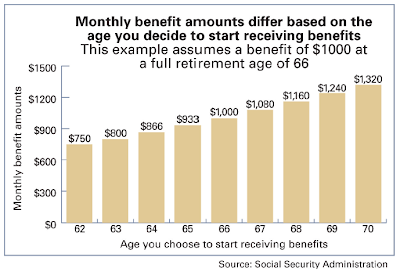

The amount you will receive depends on when you starting taking benefits. Just because you can start taking benefits at age 62 does not mean you should, especially if you plan to continue working as many boomers are planning now. Claiming Social Security benefits before the normal retirement age – currently 66 for anyone born from 1943 through 1954 – will permanently reduce those benefits by 25% for the rest of your life. Conversely, by delaying benefits after the normal retirement age you increase your benefits by 8% per year up to age 70.

For those born in 1954 or earlier, 66 is the “Magic Number” when it comes to retirement. This is the age when you can collect your full retirement even if you continue to work. There are three benefits to waiting:

1. You are entitled to full retirement benefits

2. No cap on earnings

3. You can get creative to maximize your lifetime benefits

So let’s go over some of the situations where creativity can help.

Married Couples

• In most cases, if the higher-earning spouse is relatively healthy, can afford to delay collecting benefits and the spouses are close in age, the higher-earning spouse should delay claiming Social Security for as long as possible.

• Spousal benefits are worth up to 50% of the worker’s primary insurance amount if collected at the spouse’s full retirement age; less if collected earlier. Benefits are available for spouses as early as age 62.

• If one spouse claims Social Security benefits, the other spouse can make a claim for spousal benefits only. Spousal benefits are equal to 50% of their spouse’s full benefit amount. The spouse taking the spousal benefit has to be over full retirement age and not planning to take benefits until later, ideally 70. Taking this benefit does not encroach on the benefits of the spouse taking the spousal benefit.

• If you have other retirement assets to draw on and both spouses have similar Social Security benefits and are close in age, one spouse could file and suspend their benefits while the other spouse makes a claim for spousal benefits. This way both spouses continue to accrue delayed-retirement credits and neither is encroaching on their benefits while they still collect half of one spouses monthly benefits. Win-Win!!

Widows and Widowers

• If one spouse dies and the other spouse has reached the full retirement age of 66 at that time, the surviving spouse receives 100% of the deceased's monthly retirement benefit, even if the surviving spouse collected reduced retirement benefits early. If the deceased spouse had delayed collecting retirement benefits until 70 the surviving spouse would also collect the additional benefits attributable to the four years’ worth of delayed retirement credits.

• A surviving spouse can also delay collecting their benefit until 70 while collecting their survivor benefit first.

Divorce and Social Security

• Most divorced spouses have the same rights to Social Security as if they were still married. To collect these benefits you must have been married at least 10 years, both spouses must be at least 62 years old, and the one trying to claim the benefits must be unmarried.

• The divorced spouse’s benefit is equal to up to half of the former spouse’s full retirement age amount if you begin collecting benefits at your full retirement age. If you start collecting at 62 it will only be worth 35% of the ex-spouse’s benefits.

• If your ex-spouse dies you are entitled to the same survivor benefits as if you were still married, even if your ex-spouse remarried.

Exceptions to the Rule

There are several exceptions that can reduce or eliminate the amount of your Social Security benefits.

• If you were covered under a state or municipality pension where you didn’t pay Social Security taxes, the Social Security benefits you might have earned through other employment may be limited or eliminated. This is known as the "Windfall Elimination Provision."

• Per the "Government Pension Offset," if one spouse is covered under a pension they may not be entitled to the other spouse’s full survivor Social Security benefits.

Don’t Forget the Children

• For children to be eligible for Social Security benefits, he or she must be unmarried and under 18, or under 19 if a full-time high school student. If the child becomes totally disabled before 22, they are also eligible for benefits.

• This benefit is based on 50% of the parent’s primary insurance amount at full retirement regardless of when the parent started claiming benefits.

• If the child is under 16 the spouse can also receive up to half of the worker’s retirement benefits regardless of the spouse’s age. The total amount of benefits a family can receive is capped between 150% and 180% of the worker’s full retirement benefit.

The Do-Over Strategy

• If you have reached your full retirement age, you can suspend the Social Security benefits you receive. The suspended benefits earn delayed-retirement credits. These credits are worth 8% per year for each year you postpone collecting benefits, up to age 70.

Additional resources:

SSA Bulletin - When You Should Collect Social Security

National Academy of Social Insurance - When to Take Social Security

The first baby boomers reached 65 in 2011, and the remaining 78 million people born between 1946 and 1964 will continue to turn 65 at a rate of 10,000 people per day for the next 15 years.

Social Security is the single largest source of income for the majority of Americans over 65 and represents half or more of total income for 53% of married couples and 74% of unmarried individuals. For more affluent retirement aged people, informed decisions about how and when to claim Social Security benefits can mean thousands of extra retirement income dollars per year. With the right planning a married couple could increase their lifetime income by $100,000 or more.

The amount you will receive depends on when you starting taking benefits. Just because you can start taking benefits at age 62 does not mean you should, especially if you plan to continue working as many boomers are planning now. Claiming Social Security benefits before the normal retirement age – currently 66 for anyone born from 1943 through 1954 – will permanently reduce those benefits by 25% for the rest of your life. Conversely, by delaying benefits after the normal retirement age you increase your benefits by 8% per year up to age 70.

For those born in 1954 or earlier, 66 is the “Magic Number” when it comes to retirement. This is the age when you can collect your full retirement even if you continue to work. There are three benefits to waiting:

1. You are entitled to full retirement benefits

2. No cap on earnings

3. You can get creative to maximize your lifetime benefits

So let’s go over some of the situations where creativity can help.

Married Couples

• In most cases, if the higher-earning spouse is relatively healthy, can afford to delay collecting benefits and the spouses are close in age, the higher-earning spouse should delay claiming Social Security for as long as possible.

• Spousal benefits are worth up to 50% of the worker’s primary insurance amount if collected at the spouse’s full retirement age; less if collected earlier. Benefits are available for spouses as early as age 62.

• If one spouse claims Social Security benefits, the other spouse can make a claim for spousal benefits only. Spousal benefits are equal to 50% of their spouse’s full benefit amount. The spouse taking the spousal benefit has to be over full retirement age and not planning to take benefits until later, ideally 70. Taking this benefit does not encroach on the benefits of the spouse taking the spousal benefit.

• If you have other retirement assets to draw on and both spouses have similar Social Security benefits and are close in age, one spouse could file and suspend their benefits while the other spouse makes a claim for spousal benefits. This way both spouses continue to accrue delayed-retirement credits and neither is encroaching on their benefits while they still collect half of one spouses monthly benefits. Win-Win!!

Widows and Widowers

• If one spouse dies and the other spouse has reached the full retirement age of 66 at that time, the surviving spouse receives 100% of the deceased's monthly retirement benefit, even if the surviving spouse collected reduced retirement benefits early. If the deceased spouse had delayed collecting retirement benefits until 70 the surviving spouse would also collect the additional benefits attributable to the four years’ worth of delayed retirement credits.

• A surviving spouse can also delay collecting their benefit until 70 while collecting their survivor benefit first.

Divorce and Social Security

• Most divorced spouses have the same rights to Social Security as if they were still married. To collect these benefits you must have been married at least 10 years, both spouses must be at least 62 years old, and the one trying to claim the benefits must be unmarried.

• The divorced spouse’s benefit is equal to up to half of the former spouse’s full retirement age amount if you begin collecting benefits at your full retirement age. If you start collecting at 62 it will only be worth 35% of the ex-spouse’s benefits.

• If your ex-spouse dies you are entitled to the same survivor benefits as if you were still married, even if your ex-spouse remarried.

Exceptions to the Rule

There are several exceptions that can reduce or eliminate the amount of your Social Security benefits.

• If you were covered under a state or municipality pension where you didn’t pay Social Security taxes, the Social Security benefits you might have earned through other employment may be limited or eliminated. This is known as the "Windfall Elimination Provision."

• Per the "Government Pension Offset," if one spouse is covered under a pension they may not be entitled to the other spouse’s full survivor Social Security benefits.

Don’t Forget the Children

• For children to be eligible for Social Security benefits, he or she must be unmarried and under 18, or under 19 if a full-time high school student. If the child becomes totally disabled before 22, they are also eligible for benefits.

• This benefit is based on 50% of the parent’s primary insurance amount at full retirement regardless of when the parent started claiming benefits.

• If the child is under 16 the spouse can also receive up to half of the worker’s retirement benefits regardless of the spouse’s age. The total amount of benefits a family can receive is capped between 150% and 180% of the worker’s full retirement benefit.

The Do-Over Strategy

• If you have reached your full retirement age, you can suspend the Social Security benefits you receive. The suspended benefits earn delayed-retirement credits. These credits are worth 8% per year for each year you postpone collecting benefits, up to age 70.

Additional resources:

SSA Bulletin - When You Should Collect Social Security

National Academy of Social Insurance - When to Take Social Security

No comments:

Post a Comment