A reverse mortgage sounds like a great idea. One website touts, “You can turn the value of your home into cash without having to sell the property, move out of it, or repay a loan every month!” If this sounds too good to be true, that’s because it might be. It is important to consider if the benefits outweigh the risks.

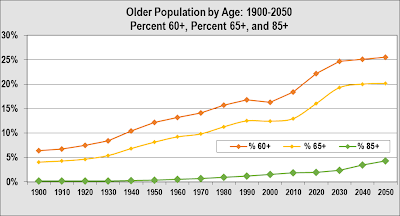

Reverse mortgages are on the rise and this trend seems likely to continue. As the percentage of the older adult population continues to increase, the lure of a reverse mortgage may become tempting for many. As you can see in the graphic below this trend has escalated in recent years and projections indicate in the next 15 years more than 25% of our population will be over the age of 60.

How a Reverse Mortgage Works – Simplified

Generally, you must be 62 years of age and occupy the home as your principal residence in order to qualify for a reverse mortgage. You must own your home outright or have a nominal mortgage balance that you can pay off with proceeds from the loan. In a traditional loan you borrow money and pay principal and interest over time to a lender to purchase a home. Conversely, a reverse mortgage pays off any existing mortgage balance and pays you a fixed monthly amount based on the equity available. In most cases with an existing mortgage they only pay the mortgage for you.

Let’s say your home is worth $250,000 and has a mortgage balance of $25,000. The reverse mortgage would pay off the $25,000 and divide the remaining equity into monthly payments of $1,000. So instead of a loan balance getting smaller like in a traditional loan, the loan balance gets larger. If you ever wanted to move or sell your home you would have to pay back the original $25,000 plus the monthly payments received plus accrued interest. The same is true if you were to die and your family wanted to keep the house. Below is a diagram illustrating the differences between a traditional mortgage and a reverse mortgage.

The only federally insured reverse mortgage loans are Home Equity Conversion Mortgages (HECMs) and to qualify for these loans your house must be a single-family home or a two- to four-unit property that you own and occupy. There are two other types of loans not federally insured, Single-Purpose Reverse Mortgage and Proprietary Reverse Mortgages, but they can have significant restrictions and much higher costs.

There are five essential questions to ask yourself before you consider a reverse mortgage:

1. Do I NEED a reverse mortgage?

2. Can I AFFORD a reverse mortgage?

3. Can I afford to start using up my EQUITY now?

4. Do I have less costly OPTIONS?

5. Do I fully UNDERSTAND how these loans work?

When we say NEED, we mean, “Will your standard of living be greatly diminished if you are unable to obtain a reverse mortgage?” Reverse mortgages are not the way to finance your dream vacation around the world or invest in the “Next Big Thing.” Reverse mortgages can be expensive and frequently have a lot of small print and special limitations. Get your glasses out and READ EVERYTHING!! If you have exhausted all of your other financial resources a reverse mortgage could be a way for you to stay in your home and have additional income.

You ask, “Why do we need to be able to AFFORD a reverse mortgage?” These loans can be very expensive and the amount you owe grows every month. The younger you are when you take out a reverse mortgage, the more the compound interest will grow. The up-front cost of these loans can make moving prohibitive if you needed to move after a few years. Depending on how the reverse mortgage is structured you may need to have enough funds available to pay off the reverse mortgage if one of you die.

The more EQUITY you use now, the less you will have later when you need it. This is especially important for future medical emergencies, healthcare needs, increases in living expenses or if your income cannot keep pace with inflation. The equity in your house should be reserved for financial emergencies, moving to assisted living or repairs and modifications to your home.

Look at your OPTIONS before deciding on a reverse mortgage. Just about any option you could imagine costs less than a reverse mortgage. If you can afford a home equity line-of-credit this is a much better solution. Utilize resources for older adults that can provide special financing for home repairs, property taxes and healthcare expenses. Have you ever considered downsizing? Moving into a smaller home sooner rather than later has been proven to increase older adults’ quality of life, or better yet, make your vacation home permanent.

UNDERSTANDING how these loans work and how they are different from traditional mortgages is the most important step in deciding if a reverse mortgage is right for you. If you enter into a reverse mortgage, in all likelihood there will be little equity in your home to leave you children after your death.

While a reverse mortgage could be a monthly source of income for you it is important to fully understand all of the risks associated with these types of mortgages. You can contact a HECM Counselor through the National Clearinghouse for Long-Term Care Needs, National Council on Aging or the Department of Housing and Urban Development to answer questions and explore additional options.

If you would like to contact the author of this article, contact Monica Tulley at 404.892.7967 or mtulley@rollinsfinancial.com

More Information:

National Clearinghouse for Long-term Care Needs

National Council on Aging

Department of Housing and Urban Development - Reverse Mortgages

Reverse mortgages are on the rise and this trend seems likely to continue. As the percentage of the older adult population continues to increase, the lure of a reverse mortgage may become tempting for many. As you can see in the graphic below this trend has escalated in recent years and projections indicate in the next 15 years more than 25% of our population will be over the age of 60.

How a Reverse Mortgage Works – Simplified

Generally, you must be 62 years of age and occupy the home as your principal residence in order to qualify for a reverse mortgage. You must own your home outright or have a nominal mortgage balance that you can pay off with proceeds from the loan. In a traditional loan you borrow money and pay principal and interest over time to a lender to purchase a home. Conversely, a reverse mortgage pays off any existing mortgage balance and pays you a fixed monthly amount based on the equity available. In most cases with an existing mortgage they only pay the mortgage for you.

Let’s say your home is worth $250,000 and has a mortgage balance of $25,000. The reverse mortgage would pay off the $25,000 and divide the remaining equity into monthly payments of $1,000. So instead of a loan balance getting smaller like in a traditional loan, the loan balance gets larger. If you ever wanted to move or sell your home you would have to pay back the original $25,000 plus the monthly payments received plus accrued interest. The same is true if you were to die and your family wanted to keep the house. Below is a diagram illustrating the differences between a traditional mortgage and a reverse mortgage.

The only federally insured reverse mortgage loans are Home Equity Conversion Mortgages (HECMs) and to qualify for these loans your house must be a single-family home or a two- to four-unit property that you own and occupy. There are two other types of loans not federally insured, Single-Purpose Reverse Mortgage and Proprietary Reverse Mortgages, but they can have significant restrictions and much higher costs.

There are five essential questions to ask yourself before you consider a reverse mortgage:

1. Do I NEED a reverse mortgage?

2. Can I AFFORD a reverse mortgage?

3. Can I afford to start using up my EQUITY now?

4. Do I have less costly OPTIONS?

5. Do I fully UNDERSTAND how these loans work?

When we say NEED, we mean, “Will your standard of living be greatly diminished if you are unable to obtain a reverse mortgage?” Reverse mortgages are not the way to finance your dream vacation around the world or invest in the “Next Big Thing.” Reverse mortgages can be expensive and frequently have a lot of small print and special limitations. Get your glasses out and READ EVERYTHING!! If you have exhausted all of your other financial resources a reverse mortgage could be a way for you to stay in your home and have additional income.

You ask, “Why do we need to be able to AFFORD a reverse mortgage?” These loans can be very expensive and the amount you owe grows every month. The younger you are when you take out a reverse mortgage, the more the compound interest will grow. The up-front cost of these loans can make moving prohibitive if you needed to move after a few years. Depending on how the reverse mortgage is structured you may need to have enough funds available to pay off the reverse mortgage if one of you die.

The more EQUITY you use now, the less you will have later when you need it. This is especially important for future medical emergencies, healthcare needs, increases in living expenses or if your income cannot keep pace with inflation. The equity in your house should be reserved for financial emergencies, moving to assisted living or repairs and modifications to your home.

Look at your OPTIONS before deciding on a reverse mortgage. Just about any option you could imagine costs less than a reverse mortgage. If you can afford a home equity line-of-credit this is a much better solution. Utilize resources for older adults that can provide special financing for home repairs, property taxes and healthcare expenses. Have you ever considered downsizing? Moving into a smaller home sooner rather than later has been proven to increase older adults’ quality of life, or better yet, make your vacation home permanent.

UNDERSTANDING how these loans work and how they are different from traditional mortgages is the most important step in deciding if a reverse mortgage is right for you. If you enter into a reverse mortgage, in all likelihood there will be little equity in your home to leave you children after your death.

While a reverse mortgage could be a monthly source of income for you it is important to fully understand all of the risks associated with these types of mortgages. You can contact a HECM Counselor through the National Clearinghouse for Long-Term Care Needs, National Council on Aging or the Department of Housing and Urban Development to answer questions and explore additional options.

If you would like to contact the author of this article, contact Monica Tulley at 404.892.7967 or mtulley@rollinsfinancial.com

More Information:

National Clearinghouse for Long-term Care Needs

National Council on Aging

Department of Housing and Urban Development - Reverse Mortgages

1 comment:

Great Blog! Worth the read!

Post a Comment